- 金币:

-

- 奖励:

-

- 热心:

-

- 注册时间:

- 2006-7-3

|

|

楼主 |

发表于 2009-3-18 15:32

|

显示全部楼层

Up and down day Posted by downtowntrader | 12/20/2005 09:11:00 PM | 0 comments »

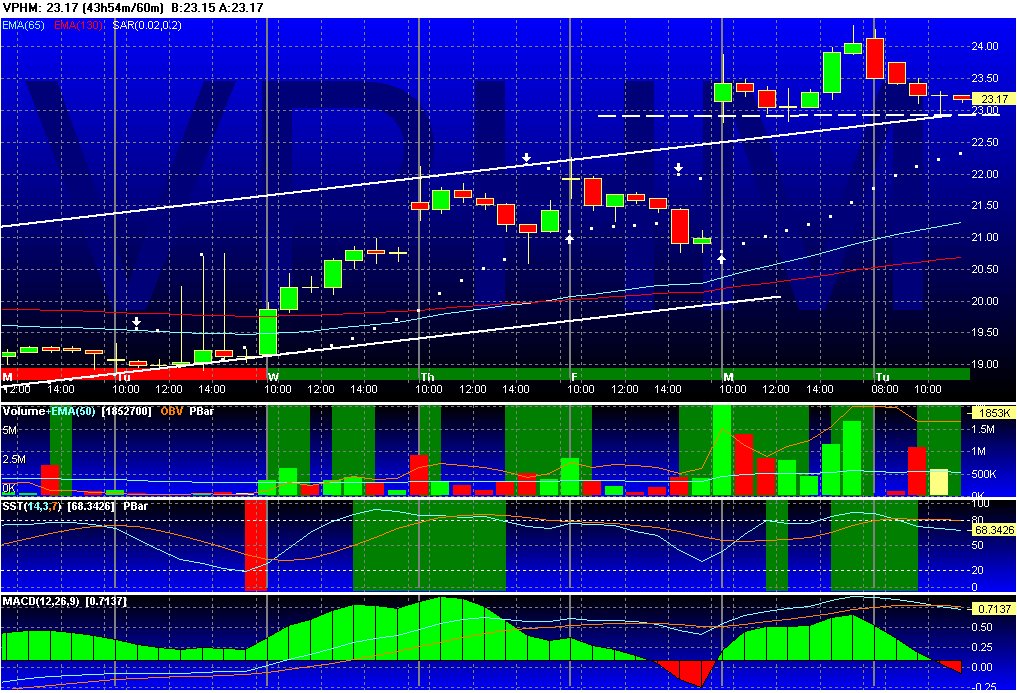

Lots of good shorts this morning, followed by some good longs in the afternoon. Hopefully some of you shorted IFO, NTAP and VPHM this morning for decent profits. I will post some charts later tonight.

DT

some charts (short side) Posted by downtowntrader | 12/19/2005 10:15:00 PM | 0 comments »

Is it time to short goog? I'm sure some piled on early today, but i would wait for a break of the trendline. Lots of negative divergences.

I was watching NTAP as a long recently, but it failed pretty badly at resistance, so it may follow through and come down to close window.

Wacthing IFO for a break of the trendline. Look at declining RSI and CMF as price is rising. Wacthing IFO for a break of the trendline. Look at declining RSI and CMF as price is rising.

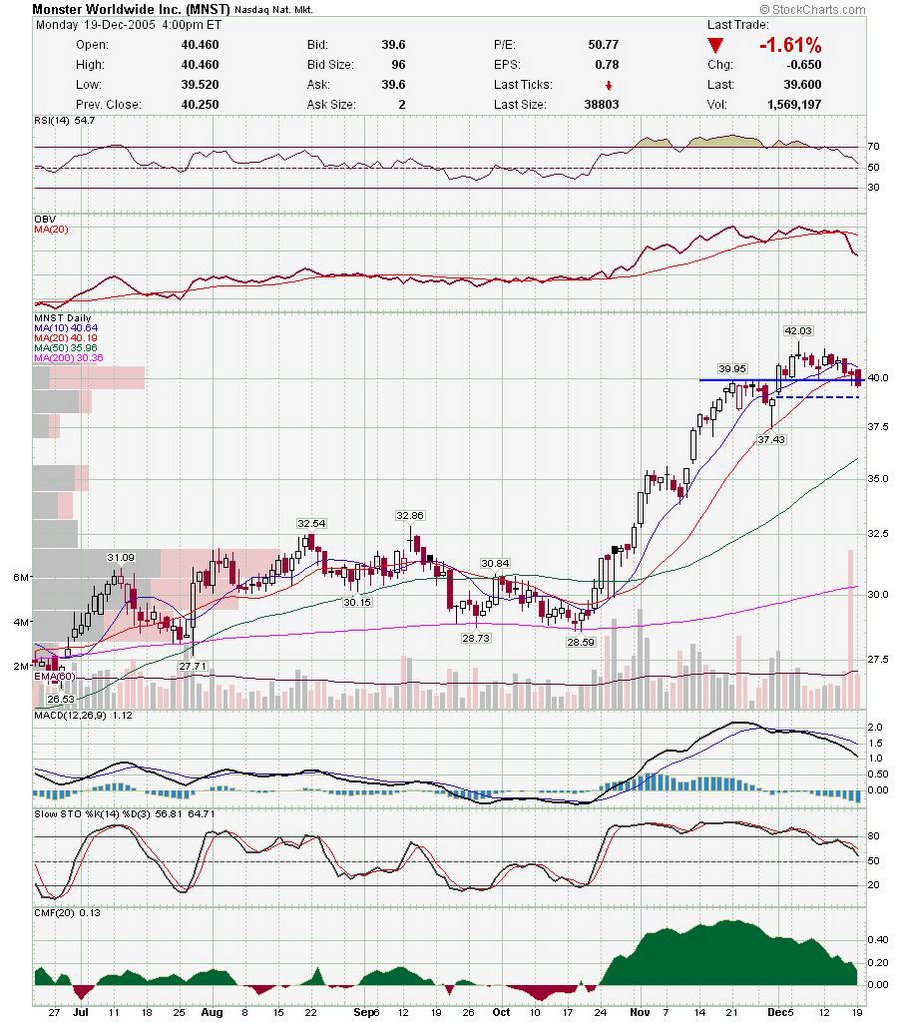

MNST is another long that failed, so it may be a short now. Has good support below but keep an eye on it. MNST is another long that failed, so it may be a short now. Has good support below but keep an eye on it.

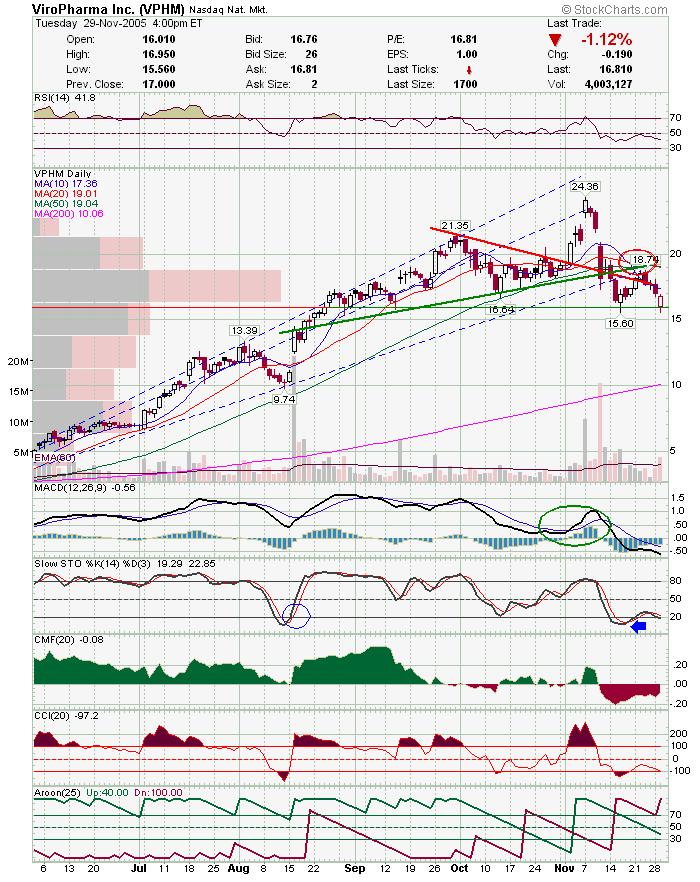

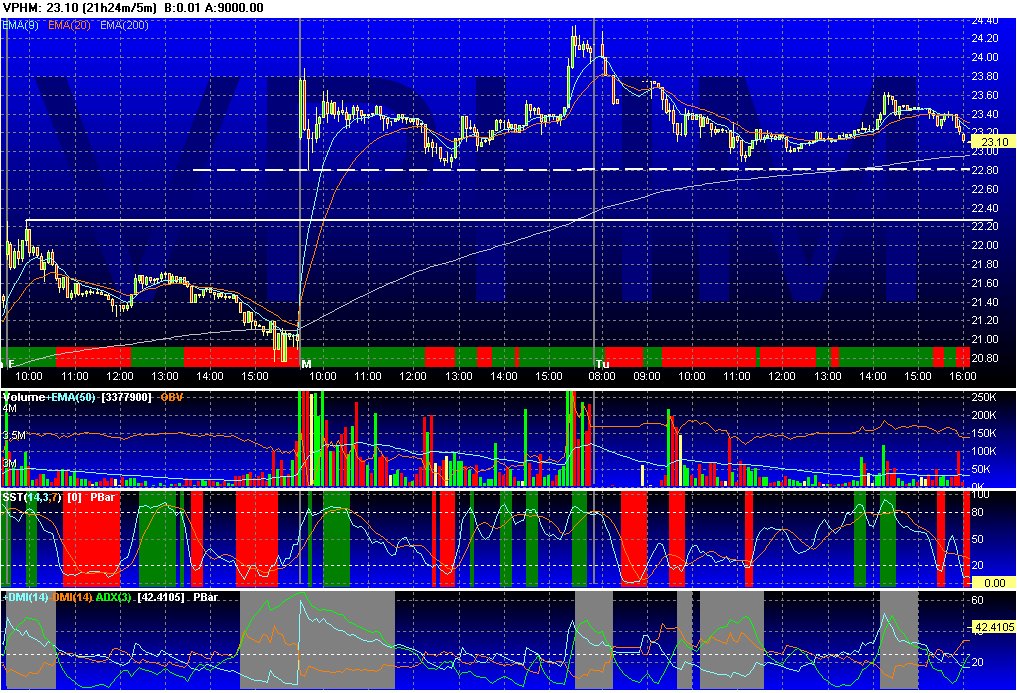

Also still watching VPHM to the short side as well. There is still a chance that we still get a rally here as the market tends to take the side of the minority, but in the real near term, we probably still need to bloody the street a little more. Be careful as volatility will surely increase in the next few days.

Good Luck,

DT

post from a board Posted by downtowntrader | 12/19/2005 10:11:00 PM | 0 comments »

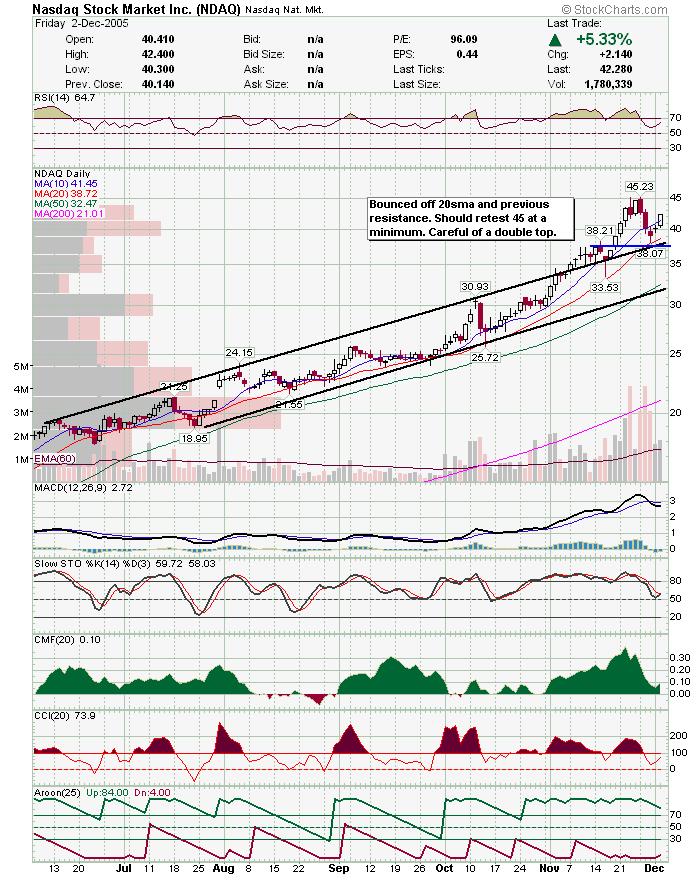

I posted this on a private board i'm on, but i thought i would post it here since it is updating some of the stocks recently on my watchlist. Basically the question was how i feel on cmed, cmt, redf, and ndaq. The links are broken but you can just cut and paste it to you address bar.

not sure what to tell you as market action trumps everything. the

nasdaq and smallcaps got hammered today and this may be the start of a

downtrend. also, i'm not sure if you own any of them or if you are

looking to get in. also, i don't know what your trading style is short

term, intermediate, etc. i'll start by saying i own cmt, cmed, and

ndaq. i was looking for redf to pullback, but this was a little steep.

i don't think i will initiate many long positions until the markets

show some strength.

cmed: had a really good move this morning and it all fell apart. i'm a

little upset that i didn't take some off the table here cause it

dropped below my buy point for a little while. It dropped from over

35-32.12 in one hour. At least it closed over the trendline. I would

hold this depending on your shares until it breaks the lower

trendline. Also, if you can watch it, i recommend mental stops on

cmed. they are one of the more volatile stocks i've traded.

http://stockcharts.com/def/servlet/SC.web?c=cmed,uu[r,a]daclyyay[dc][pb10!b20!b50!b200!i!f][vc60][iut!ub14!la12,26,9!lh14,3!lc20][j64802581,y]&listNum=13

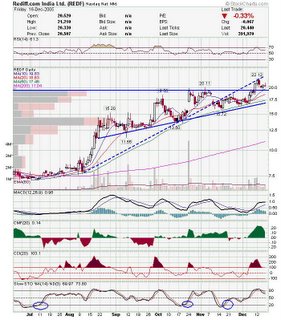

rdef: this has been a strong little stock, but it fell apart today. i

am waiting to see what happens here. it could bounce off the 20, but i

think the general markets would have to be strong for this to happen.

it may be headed back to the trendline and or 50 sma. if you own this

i would either lighten up and look to buy back at the 50 (depending on

confirmation), or hold as long as it maintains the trendline.

http://stockcharts.com/def/servlet/SC.web?c=REDF,uu[w,a]daclyyay[dc][pb10!b20!b50!b200!i!f][vc60][iut!ub14!la12,26,9!lc20!ld20!lh14,3][J59882709,Y]&listNum=4

ndaq: this was one of the stocks that held it's own when the markets

started tanking. it is still below resistance, so at this point i

don't know that i would be a buyer, but this was pretty oversold and

may still move a little higher. i am hoping for a decent pop to sell

half my position, and I plan to hold half a few more days to see what

develops.

http://stockcharts.com/def/servlet/SC.web?c=ndaq,uu[w,a]daclyyay[dc][pb10!b20!b50!b200!i!f][vc60][iut!ub14!la12,26,9!lh14,3!lc20!ld20!lv25][J64142740,Y]&pref=G

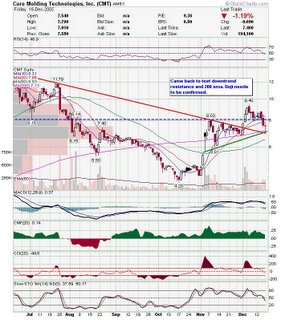

cmt: this is another stock that just didn't move when everything

around it was coming down. they also closed at high of day so that is

pretty decent. the negative is that they barely closed higher then the

close from 2 days ago, but i guess it wasn't a bad candle taking into

account the negative bias today.

http://stockcharts.com/def/servlet/SC.web?c=CMT,uu[w,a]daclyyay[dc][pb10!b20!b50!b200!i!f][vc60][iut!ub14!la12,26,9!lc20!ld20!lh14,3][J63629567,Y]&listNum=4

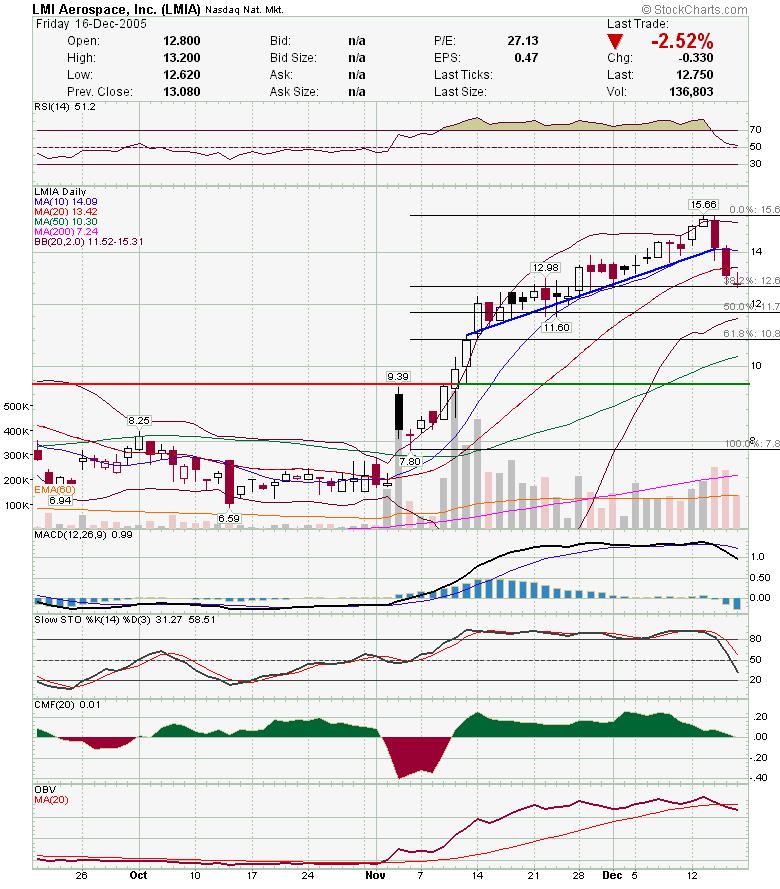

some others that held up today.

lmia, nwre, and ntri.

hope this helps.

good luck,

dt

A few charts to look at Posted by downtowntrader | 12/18/2005 11:04:00 PM | 0 comments »

Here are a few interesting charts.

LMIA: Doji at the 38.2% retrace and previous resistance. Wait for confirmation, but this has been a very strong stock.

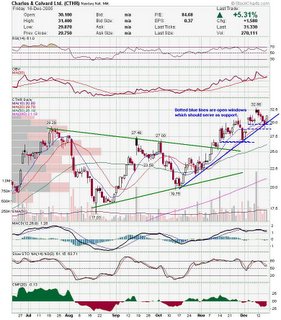

CTHR:Nice move Friday off the trendline. Nice support below. CTHR:Nice move Friday off the trendline. Nice support below.

REDF: Careful with this one as it may be in b of an Elliot Wave abc correction. I would love for this to fall near the 20 sma, but will be watching for a breakout. REDF: Careful with this one as it may be in b of an Elliot Wave abc correction. I would love for this to fall near the 20 sma, but will be watching for a breakout.

CMT: Read comments on chart. CMT: Read comments on chart.

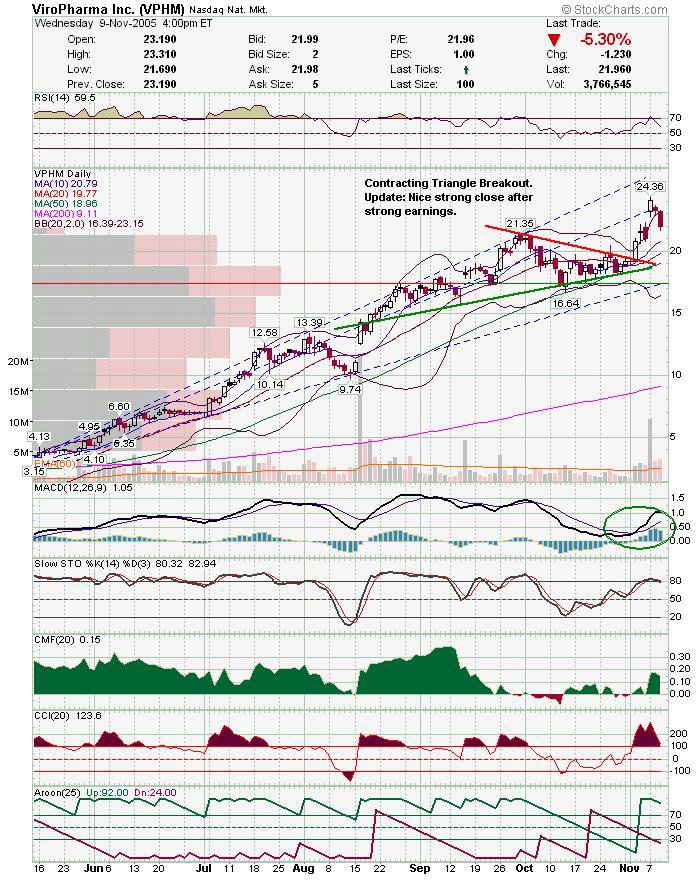

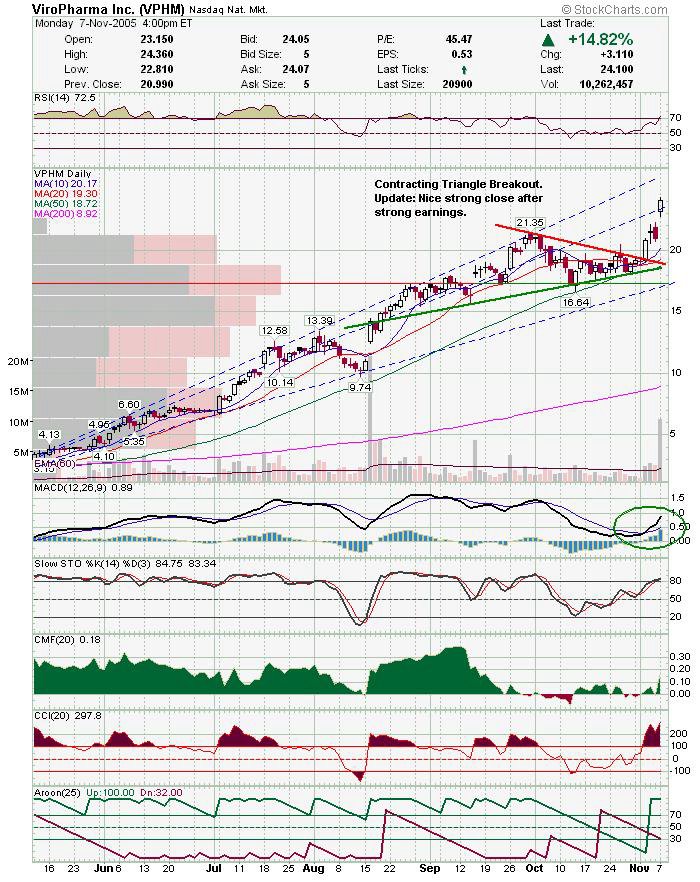

VPHM has been steadily climbing but has been quietly struggling with a trendline that was previous support. I am watching this for an attempt to close the window (gap) above. If it falters, may be a decent short.

NDAQ: Read chart notes. This could make a decent daytrade as well as a swing, as volume is ok and there is a decent target near the red downtrend line. NDAQ: Read chart notes. This could make a decent daytrade as well as a swing, as volume is ok and there is a decent target near the red downtrend line.

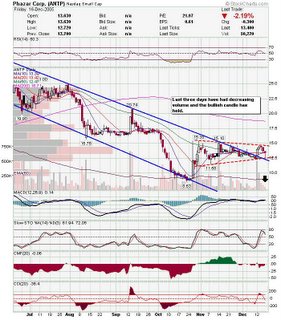

ANTP: Retested support and held. I will enter if it makes a higher high tomorrow. ANTP: Retested support and held. I will enter if it makes a higher high tomorrow.

CMED: CMED looks like it broke the triangle Friday, but pulled back slowly on decreasing intraday volume. I am showing a fib fan of the most recent leg up. Cmed is currently on the 61.8% retrace and could follow this fan line up. CMED: CMED looks like it broke the triangle Friday, but pulled back slowly on decreasing intraday volume. I am showing a fib fan of the most recent leg up. Cmed is currently on the 61.8% retrace and could follow this fan line up.

Also on my list Also on my list

BCON: Very weird close friday with a huge buy at 4:00pm. (no options on them)

MNST: Looks like the may have succesfully tested support

SNTO

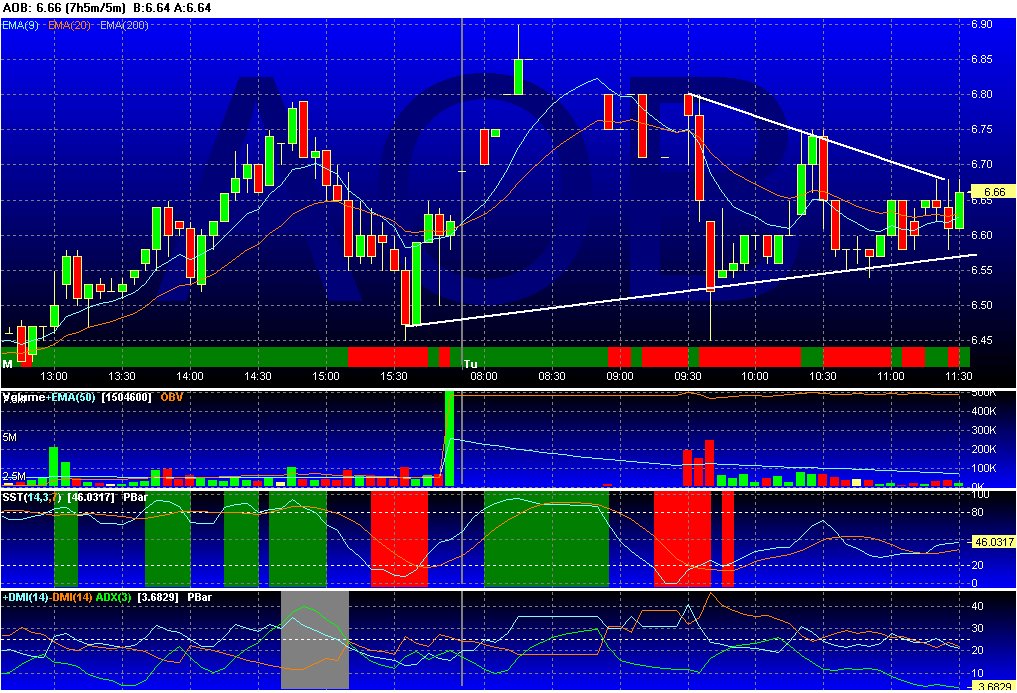

AOB

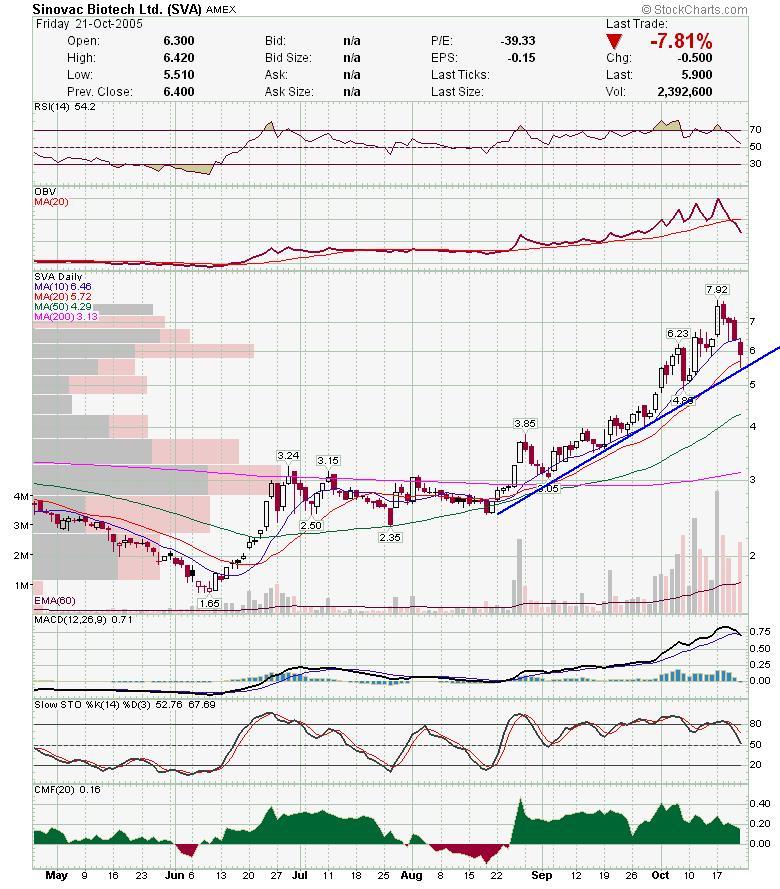

SVA

FFIV

MRVL

RNWK

QDEL: I think bottom is in. Should pop up a little and come back and retest.

Good Luck,

DT

Fibonacci Fans Posted by downtowntrader | 12/18/2005 06:36:00 PM | 0 comments »

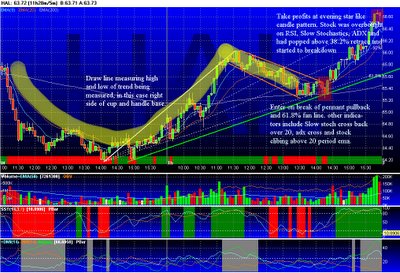

Fibonacci Fans are one of the tools I use to try and find areas of support and resistance to either go long or take profits. I try to find areas where support or resistance would normally be found, as well as look for a convergence of signals from my indicators. Here is an example of a trade I took where almost everything lined up very nicely. HAL had closed while forming a double bottom. The next day it built the right side of a cup and handle (shown in yellow) on the intraday 5 minute chart. I started watching it as it was pulling back and forming the handle. Since the low and high were defined at that point, I drew a line connecting the two, and looked at the fibonacci fans it formed. If your platform doesn't support fibonacci tools, I recommend looking at medved quotetracker. It has a free version as well. It looked like HAL was respecting the fib fans on the pullbacks so I watched as it pulled back after lunch. Everything came together where I drew the red square. First HAL started finding support at the 200 period ema. Second, the Slow Stochastics crossed back into normal territory from oversold. There was an ADX crossover and HAL reclaimed the 20 period ema at the same time it was breaking the resistance line from the pullback (shown in orange). The fib fan confirmed everything as it was a 61.8% retrace. The fib fan also accurately showed resistance at the 50% and then the 38.2%. The other factor which is often overlooked is what time all this happened. I have much more faith in a breakout starting at 2:00pm then sometime between 11:30 and 1:00. One could of taken partial profits once HAL started to fight with the 50% retrace but it never seriously threatened the 20 period ema after it broke out. The trade was closed after it pulled over the 32.8% fan line and then formed an evening star like pattern. It was also near 4:00pm, so it was a convenient exit.

I use fib. fans almost exclusively on intraday charts but once in a while check it on daily charts. Here is an example of the Nasdaq composite showing a fib. fan. There is some subjectivity as to where the high and low of the trend are, and I chose the first high here, before it started trading sideways. The composite has been trading sideways for about 17 days now and should start a move to either direction soon. The bollinger bands are tight and the 10 and 20 period sma's have converged with an ascending trendline. I am looking to the fib fans as potential support if it breaks down. I use fib. fans almost exclusively on intraday charts but once in a while check it on daily charts. Here is an example of the Nasdaq composite showing a fib. fan. There is some subjectivity as to where the high and low of the trend are, and I chose the first high here, before it started trading sideways. The composite has been trading sideways for about 17 days now and should start a move to either direction soon. The bollinger bands are tight and the 10 and 20 period sma's have converged with an ascending trendline. I am looking to the fib fans as potential support if it breaks down.

Now an important observation I haev made, is that fib fans don't act as classic trendlines do. They are more like magnets and the stock tends to trade around them. So if it breaks one it will either trade a few days hugging the opposite side of the line, or it will fall back (or up) near the next line. I never rely on just fib fans, but they are useful if you are looking to confirm your own trendlines or indicator analysis. Good Luck out there, Now an important observation I haev made, is that fib fans don't act as classic trendlines do. They are more like magnets and the stock tends to trade around them. So if it breaks one it will either trade a few days hugging the opposite side of the line, or it will fall back (or up) near the next line. I never rely on just fib fans, but they are useful if you are looking to confirm your own trendlines or indicator analysis. Good Luck out there,

DT.

I will post an update on what I'm watching later tonight.

DSL problems Posted by downtowntrader | 12/16/2005 12:24:00 PM | 0 comments »

Sorry for the lack of an update last night.. I'm having DSL problems. Check out CMED from my earlier post this week, as I think they are poised to break out of the triangle today. Also, NDAQ may be ready to move from the recent touch of the 50 day sma, NILE broke out, and QDEL looks like it is bottoming out.

Good Luck,

DT

Some charts Posted by downtowntrader | 12/14/2005 09:58:00 PM | 0 comments »

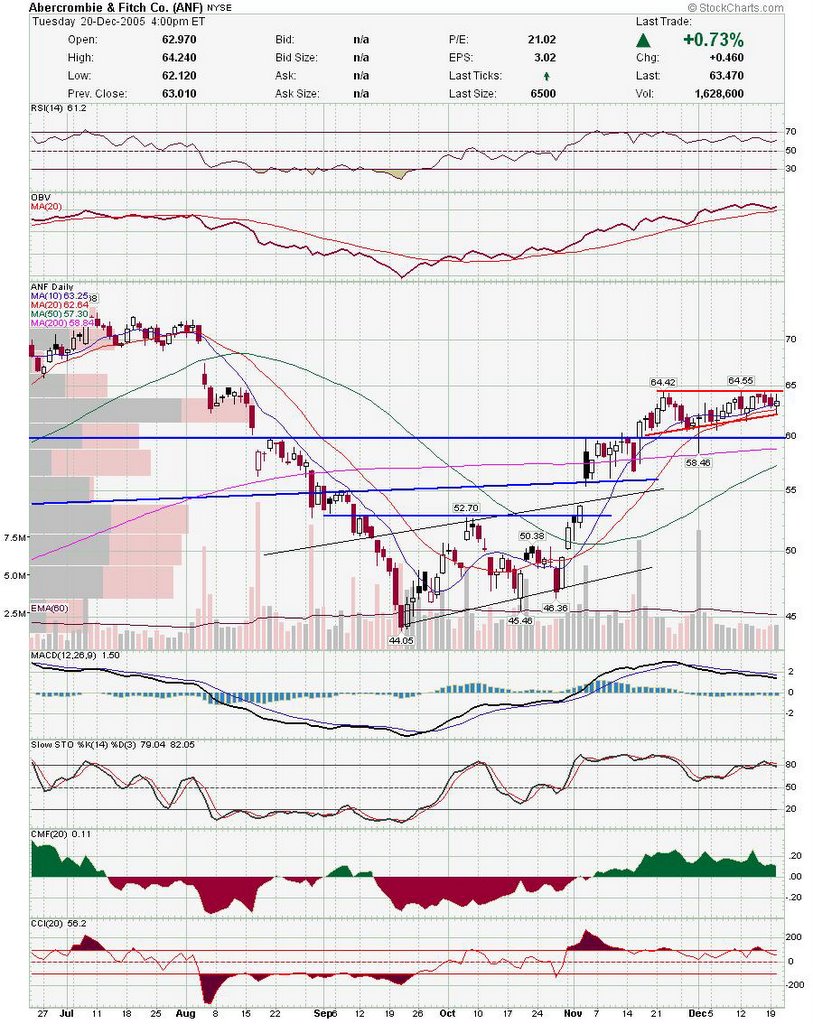

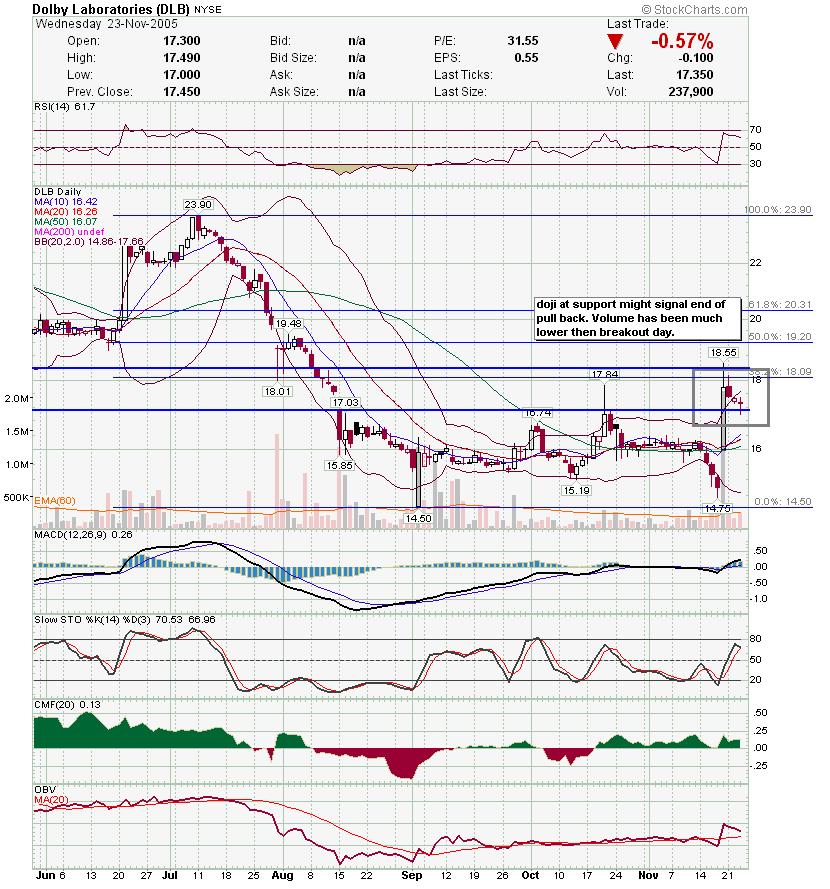

I had a few good ones on my list from last night including ENG, CKCM and YHOO. Too bad RHAT was upgraded overnight as I didn't get a chance to enter. Here are a few on my list for tomorrow. Other's on my list not listed below include DLB, PWR, SNTO, VLO, ANF, and NTAP.

CMED: This is probably tops on my list.

IFO: May hold the trendline. IFO: May hold the trendline.

TRAD: looking for a bounce off the trendline here. TRAD: looking for a bounce off the trendline here.

NILE: Finding support on the blue line. Should try and close the window in between the dotted blue lines. NILE: Finding support on the blue line. Should try and close the window in between the dotted blue lines.

NDAQ: May of sold off too hard, and may be ripe for a bounce off the 50. NDAQ: May of sold off too hard, and may be ripe for a bounce off the 50.

Update Posted by downtowntrader | 12/14/2005 08:34:00 AM | 0 comments »

These are on my watchlist today, although I probably won't trade much today if the markets don't pick a direction.

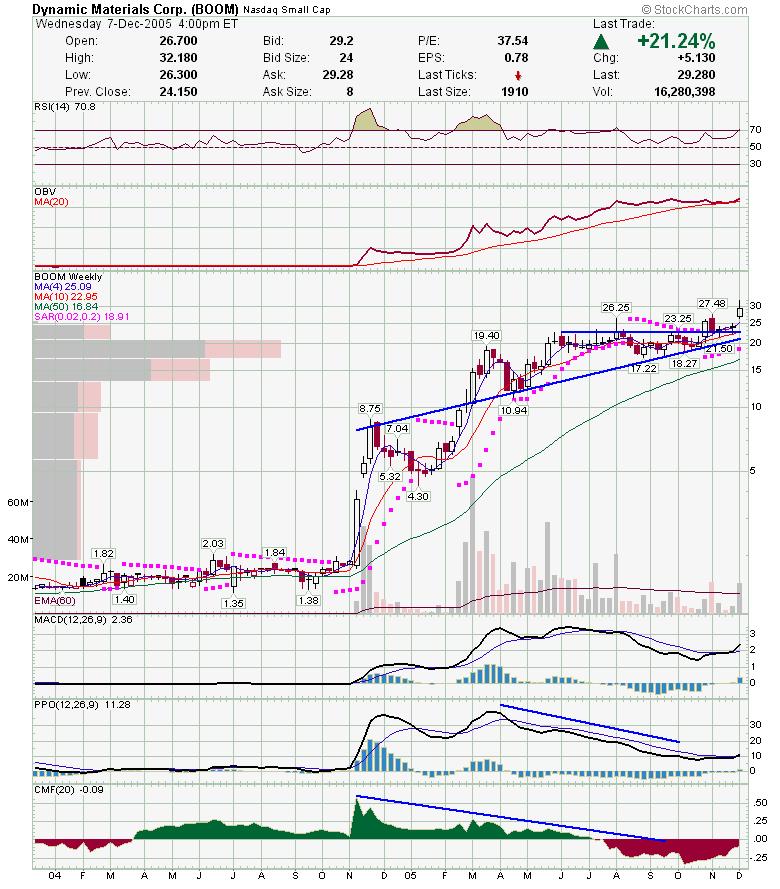

boom

swings

rhat

ffiv

eng

ckcm

slw

dna

gild

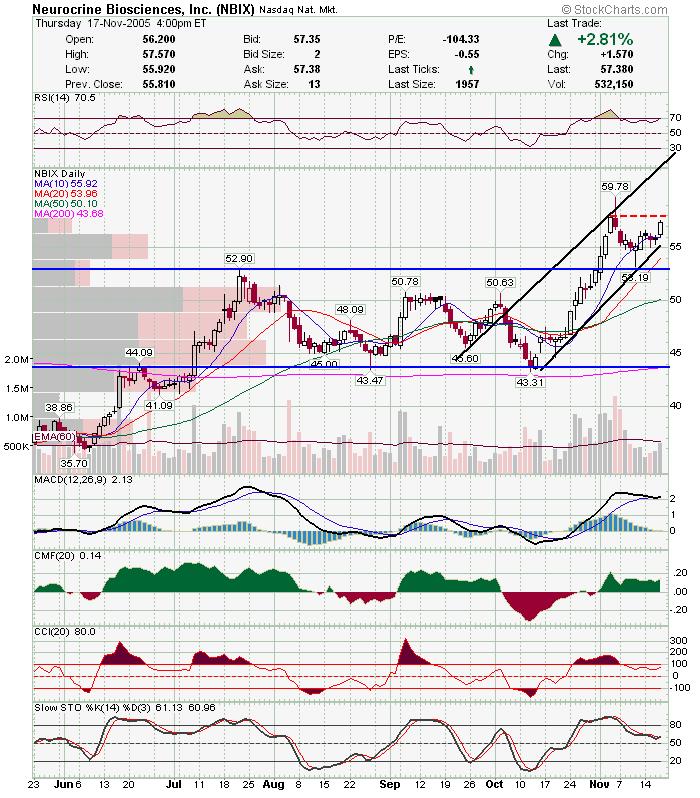

nbix

sva

cmt

haup

snto

daytrades

amzn

yhoo

grmn

sbux

pnra

vphm |

|

|

[复制链接]

[复制链接]